The weight of high-interest consumer debt is a pressing crisis for many property owners. With the average credit card Annual Percentage Rate (APR) hovering around 20 percent. Carrying a revolving balance can make true debt reduction feel impossible. If you own a home, you face a pivotal financial decision: Do you leverage your home’s value for cheaper debt, or do you pursue formal credit card forgiveness?

This choice determines whether your debt remains unsecured (protected from foreclosure) or becomes secured (placing your home at risk). For homeowners seeking a definitive reset, understanding the tax, credit, and legal implications of formal credit card forgiveness, from negotiating a settlement to filing for bankruptcy, is essential before risking the equity you’ve worked hard to build.

This guide simplifies the complex trade-off between secured savings and unsecured protection, helping you decide which path is right for your financial future.

Path 1: Using Home Equity to Slash Interest Rates

For homeowners with stable income, tapping into home equity is the fastest way to replace high-cost credit card debt with low-cost financing.

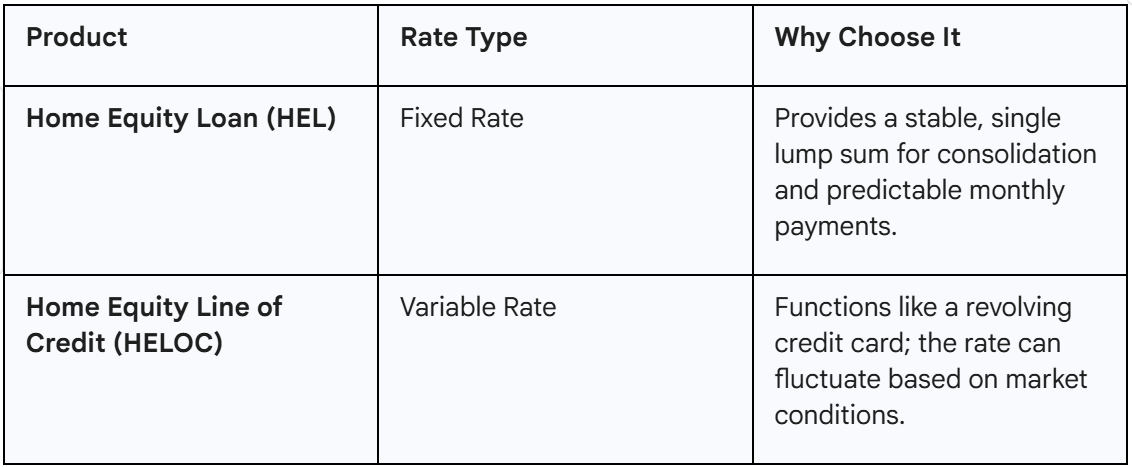

The Advantage: Low Secured Rates

By using your property as collateral, you can access interest rates dramatically lower than the 20% average credit card APR. As of late 2025, home equity products are available below 8.5 percent, with fixed-rate Home Equity Loans (HELs) averaging around 7.99% for well-qualified borrowers.

Eligibility and the Foreclosure Warning

To qualify for the best rates, lenders require strong financial health: a credit score of 680 or above and at least 20% equity in your home (80% Loan-to-Value, or LTV).

The Major Risk: When you use home equity for debt, you turn unsecured debt (which is safe from foreclosure) into secured debt. If you fail to make payments on the HEL or HELOC, you put your primary residence at direct risk of foreclosure. This strategy is only safe if your income is completely secure.

Path 2: Formal Credit Card Forgiveness

When debt is overwhelming and the idea of securing it against your home is too risky, formal credit card forgiveness offers legal or negotiated relief, preserving the unsecured status of your property.

1. Short-Term Relief: Hardship Programs

If you face a temporary crisis (e.g., job loss, serious illness), you can often negotiate directly with your credit card issuer. Hardship programs are typically unadvertised but allow for temporary payment pauses, fee waivers, or reduced interest rates. You must provide documented proof of your hardship to qualify.

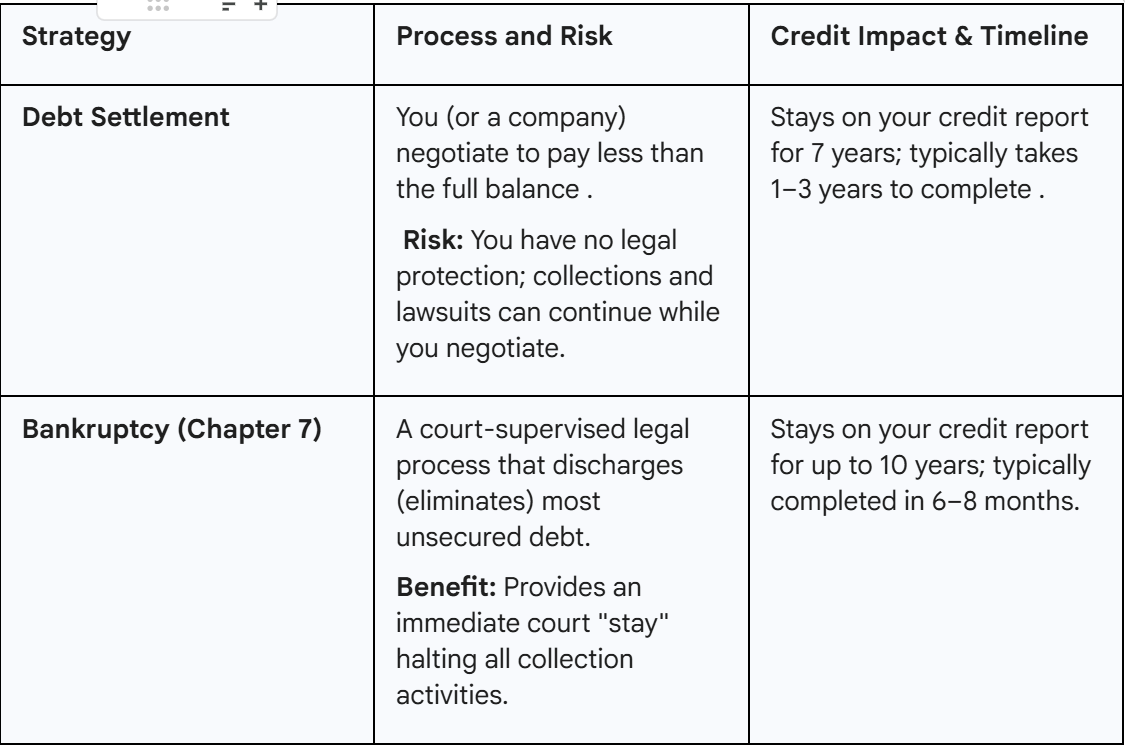

2. Negotiation vs. Legal Action

For systemic debt problems, you face two main options:

For immediate protection and certainty, bankruptcy is often the safer choice for a deep financial crisis. Learn how to vet debt relief programs and avoid scams.

Avoiding the Tax Trap on Forgiven Debt (Form 1099-C)

One of the most critical warnings regarding credit card forgiveness is the potential tax bill. The IRS generally considers any canceled debt of $600 or more to be taxable income. Your creditor will send you and the IRS a Form 1099-C (Cancellation of Debt).

To avoid paying taxes on the forgiven amount, you must qualify for an exclusion and file IRS Form 982:

- Bankruptcy Exclusion: Debt discharged through bankruptcy is automatically excluded from taxable income. This is the guaranteed tax shield.

- Insolvency Exclusion: If debt is settled outside of bankruptcy, you can exclude the income if you can prove you were "insolvent" immediately before the cancellation. This means your total liabilities exceeded the fair market value of your total assets.

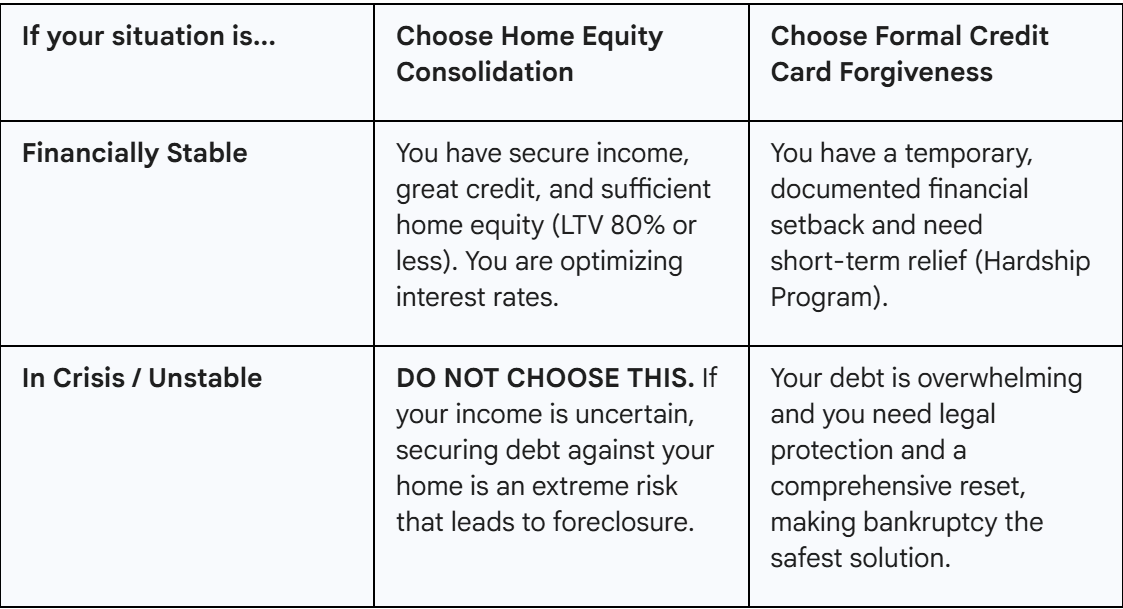

Final Choice: When to Consolidate vs. Forgive

The decision framework is simple: Are you trading unsecured debt for secured debt purely for interest savings, or out of desperation?

Final Recommendations and Next Steps

The goal is always to address the root cause of the debt and create a plan to avoid future re-accumulation.

- Seek Professional Guidance: Before moving forward with home equity or credit card forgiveness, consult a financial advisor or a HUD/NFCC-certified credit counselor for impartial advice.

- Protect Your Home: If you foresee any risk of mortgage delinquency or foreclosure, do not increase your secured debt burden. The ability to use credit card forgiveness to discharge debt in bankruptcy while keeping the home protected is invaluable.

- Explore Options: If selling your home is the only way to resolve overwhelming debt, Discover how to unlock your home equity and learn how a sale-leaseback can help you address the issue with no added debt and a structured plan

Real estate innovator and Managing Partner at PIA Residential and Sell2Rent, boasting over 20 years of experience and 2,000+ units acquired. A Wharton MBA and Forbes contributor, he brings institutional-grade authority to every market insight he shares. Danny’s expertise is further validated by his role on the Planning and Zoning Board for the City of Hallandale, where he helps shape the local landscape. For readers seeking credible, battle-tested advice, Danny offers the perspective of a leader who has successfully navigated decades of market cycles.

Subscribe to the Real Estate Digest. Weekly newsletter.