For generations, the American Dream was drawn with a single, unmistakable image: a house, a yard, a mailbox with your name on it. Ownership was security. Ownership was arrival. But in 2026, that image is being redrawn and for a growing number of Americans, the dream has quietly become a burden.

Rising insurance premiums, unpredictable maintenance costs, sky-high mortgage rates, and a housing market still stubbornly resistant to correction have combined to produce something economists are watching closely: a generational pivot away from ownership and toward intentional renting. Not renting as a stepping stone, renting as a destination.

The Hidden Price Tag Nobody Told You About

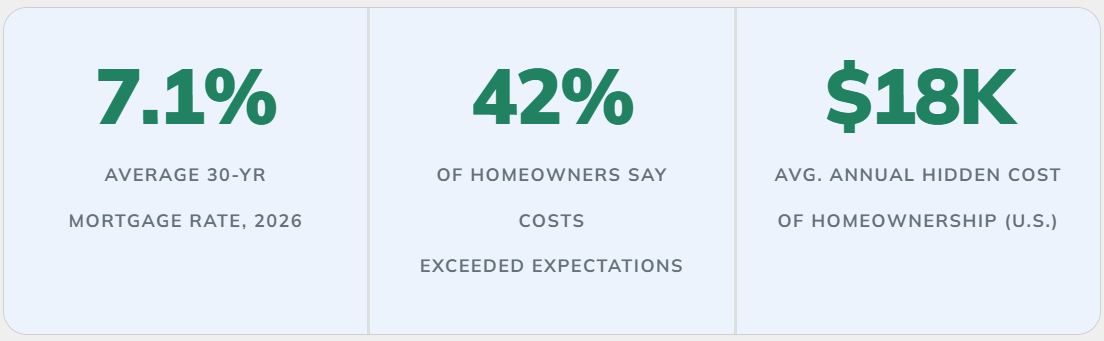

When people calculate whether they can "afford" a home, they almost always anchor on the mortgage payment. But the true cost of homeownership what Bankrate calls the "invisible bill" is dramatically larger. Property taxes, homeowner's insurance (now rising faster than inflation in wildfire and flood-prone states), HOA fees, routine maintenance, and unexpected repairs can collectively add tens of thousands of dollars annually to a home that looks perfectly affordable on paper.

A Zillow Research analysis found that when you layer in all ownership costs, many homeowners in mid-tier markets are paying a significant premium over what a comparable rental would cost without the flexibility, and with far more risk concentrated in a single illiquid asset.

The Rate Trap: Locked In, Locked Out

The mortgage rate environment has created two distinct classes of American homeowner. The first group purchased before 2022 and holds Federal Reserve-era sub-3% mortgages they would never willingly surrender. The second group, buyers, who entered the market in the last three years are paying rates between 6.5% and 7.5%, dramatically compressing their disposable income and long-term wealth-building capacity.

This "golden handcuff" effect has frozen the resale market. Existing owners won't sell because they'd lose their rate. New buyers can barely qualify. The result: record-low inventory, prices that refuse to fall, and a locked market in which the only rational move, for many, is to step back entirely.

Climate Risk Is Now a Financial Risk

There is a third, newer force accelerating the retreat from ownership: climate. Homeowners insurance is becoming unaffordable or outright unavailable in large swaths of California, Florida, Texas, and Louisiana. States like California have seen major insurers exit the market entirely. The actuarial math on wildfire, flood, and hurricane risk has fundamentally changed and homeowners are absorbing the full cost.

For many families in high-risk corridors, owning a home in 2026 no longer means building wealth. It means holding concentrated, unhedged exposure to climate catastrophe on top of all the other financial risks ownership already carries.

The Lifestyle Renter Is Not Who You Think

The popular image of a renter, young, transient, unable to buy, is badly out of date. U.S. Census Bureau data shows a fast-growing segment of renters who are older, wealthier, and choosing to rent deliberately. They have the down payment. They have the credit. They simply prefer liquidity, flexibility, and freedom from the responsibilities of ownership.

This is the rise of the lifestyle renter: professionals who value geographic freedom; retirees who don't want to be tied to a property; families who want to live in neighborhoods they couldn't otherwise afford to own in. For them, renting isn't a consolation prize. It's a portfolio strategy.

So What About the Equity You've Already Built?

For existing homeowners sitting on significant equity, the question isn't simply "should I sell?" It's "what do I do with my equity while I live life on my own terms?" Selling outright means relinquishing a long-term asset. Not selling means staying anchored. This is the tension that most financial advisors can't resolve cleanly and precisely the gap that innovative real estate solutions are stepping into.

Sell2Rent: The Bridge Between Ownership and Freedom

Sell2Rent has emerged as one of the most practical and trusted solutions for homeowners who want to unlock their equity without uprooting their lives. The concept is elegantly simple: sell your home at off-market value, access your equity, and remain in the property as a renter on your terms, on your timeline.

It's not a loan. It's not a reverse mortgage. It's a genuine sale with a genuine leaseback. Giving you liquidity, stability, and the freedom to redirect your wealth without the chaos of a traditional move. In a market defined by complexity and anxiety, Sell2Rent cuts through with unusual clarity and transparency.

For homeowners facing the 2026 crossroads, too much equity locked up, too much uncertainty about what comes next, it's a third path most people didn't know existed.

Is This a Permanent Shift or a Cycle?

Skeptics will note, correctly, that American housing has always been cyclical. Rates will come down. Inventory will loosen. The calculus will shift. But what's different in 2026 is that the cultural pressure to own, the moral weight of it, the social status attached to it, is weakening in ways that feel structural rather than cyclical.

Younger Americans who watched their parents experience 2008 are not romanticizing ownership the way prior generations did. Pew Research Center data on generational attitudes shows a meaningful and persistent decline in the belief that buying a home is always the best financial decision a person can make.

When culture changes, markets follow. Build-to-rent communities are expanding rapidly. Institutional investment in single-family rentals has professionalized the rental experience. The infrastructure of a high-quality rental lifestyle is being built in real time and platforms like Sell2Rent are making the transition seamless and financially intelligent for existing homeowners.

The New Math of a Well-Lived Life

None of this is to say that ownership is wrong, or that renting is universally superior. Personal finance is personal. Geography matters. Family stage matters. Time horizon matters. But what 2026 has brought into sharp focus is that the old calculus "renting is throwing money away," "your home is your best investment" is far less universal than we pretended it was.

For a homeowner sitting on $300,000 in equity in a house that costs $2,400 a month to own but could rent for $1,900, the numbers tell a compelling story. Deployed conservatively, that equity could generate meaningful monthly income. The ownership premium disappears. The flexibility appears. And suddenly, lifestyle over liability isn't an abstract value statement, it's arithmetic.

The burden of owning is real. So is the possibility of something lighter. In 2026, more Americans than ever are choosing to set it down and discovering, with some relief, that freedom can be a very sound financial strategy. For those ready to take that step, Sell2Rent offers a transparent, proven, and human path forward.

Real estate innovator and Managing Partner at PIA Residential and Sell2Rent, boasting over 20 years of experience and 2,000+ units acquired. A Wharton MBA and Forbes contributor, he brings institutional-grade authority to every market insight he shares. Danny’s expertise is further validated by his role on the Planning and Zoning Board for the City of Hallandale, where he helps shape the local landscape. For readers seeking credible, battle-tested advice, Danny offers the perspective of a leader who has successfully navigated decades of market cycles.

Subscribe to the Real Estate Digest. Weekly newsletter.