As the calendar turns to January 2026, many American households are waking up to a sobering financial reality: a record-breaking $1.33 trillion in credit card debt. According to recent Federal Reserve data, revolving credit has surged as families lean on plastic to navigate the persistent "cost-of-living" squeeze.

After a 2025 holiday season fueled by high prices and static wages, the "holiday hangover" has become a chronic condition. For many, the standard advice to "just budget better" feels out of touch when average credit card APRs are stuck near 23%, despite marginal Fed rate cuts. This isn’t just debt; it’s a "Golden Handcuff" scenario where your income is siphoned off to pay for the past, leaving nothing for your future.

But what if the solution wasn't found in your paycheck, but in the four walls around you? In 2026, homeowners are increasingly turning to a strategic move to reset their finances: the Sell2Rent leaseback.

The 2026 Debt Landscape: By the Numbers

The financial environment of early 2026 is uniquely challenging. While the Federal Reserve has begun a cycle of rate reductions, Bankrate’s 2026 forecast notes that card issuers have been slow to lower APRs, keeping the "interest tax" at historic highs.

- Total National Credit Card Debt: ~$1.33 Trillion.

- Average Household Balance: Over $11,000, per recent TransUnion projections.

- The Interest Trap: At a 23% interest rate, making only the minimum payment on an $11,000 balance could take over 20 years to pay off and cost you nearly $15,000 in interest alone.

This math is the primary reason American families feel stuck. As CBS News reports, the spread between what you earn in savings (4–5%) and what you pay on debt (20%+) makes it virtually impossible to "save" your way out of a hole.

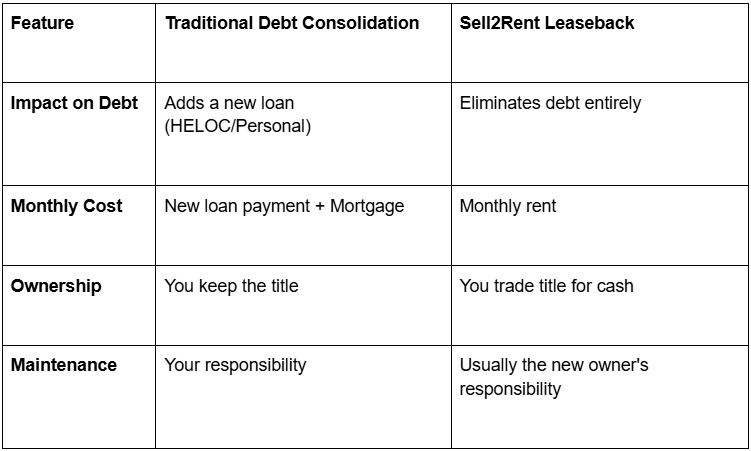

Why Traditional Debt Solutions are Falling Short

In previous years, a homeowner might look to a Home Equity Line of Credit (HELOC) or a Cash-Out Refinance. However, 2026 presents two major hurdles:

- Tightened Lending Standards: As noted in the 2026 Banking Outlook from Deloitte, banks have tightened underwriting due to rising credit losses. If your score has dipped due to high debt utilization, you may not qualify for the best rates.

- The "Rate Lock" Effect: Millions of homeowners are sitting on 3% or 4% mortgages from the early 2020s. Trading that low rate for a 2026 market rate just to get cash out often increases your total monthly housing cost significantly.

The 2026 Strategy: Unlock Equity without the Debt

This is where the Sell2Rent leaseback model is changing the game. Unlike a loan, a sale-leaseback is a real estate transaction that allows you to convert your home’s equity into cash without taking on a new monthly interest payment to a bank.

How Sell2Rent Works

Through Sell2Rent, the process is straightforward:

- Sell Your Home: You sell your property to an investor at a fair market price.

- Unlock Your Cash: You receive your equity in a lump sum enough to wipe out that $1.33 trillion national debt statistic from your personal balance sheet.

- Stay as a Tenant: You sign a lease to stay in your home as a renter. No moving trucks, no changing school districts, and no saying goodbye to your neighborhood.

The Benefits of a Clean Slate

- Immediate Debt Liquidation: Imagine waking up tomorrow with $0 in credit card debt. Your credit score would likely skyrocket as your utilization drops to zero.

- Predictable Expenses: As a renter in a leaseback, you are typically no longer responsible for property taxes, homeowners insurance, or major structural repairs, costs that NAR economists expect to continue rising in 2026.

- Financial Agility: You trade a non-liquid asset (home equity) for liquid cash that can be used to shore up your retirement or emergency fund.

Is a Leaseback Right for You?

While the prospect of a "clean slate" is enticing, it’s important to weigh the pros and cons.

Pro Tip: A leaseback is ideal for those who are "house rich but cash poor." If you have significant equity but struggle to make ends meet due to 23% APR interest, this strategy provides the exit ramp you've been looking for.

Frequently Asked Questions

Will I be evicted if I sell to a leaseback company?

No. The core of a Sell2Rent agreement is the lease. This is a legally binding contract protected by Truth in Lending and Consumer Leasing rules that guarantees your right to stay in the home for the duration of the lease term.

How much of my home's value can I get?

Most sale-leaseback programs allow you to access85% your home but they will buy you home “as-is” which means no repairs or market ready investment which can mean 5-10% of the home value depending of the need, minus any remaining mortgage balance and transaction fees. This is often more capital than a bank loan, which typically caps borrowing at 80% of the home's value.

What happens to my credit score?

Paying off high-interest credit cards is one of the fastest ways to improve a credit score. By using the proceeds from a Sell2Rent transaction to zero out your balances, you are effectively removing the "debt drag" from your credit profile instantly.

Start Your Year with a Clean Slate

The "Golden Handcuffs" only stay on if you keep the key in your pocket. As we navigate the financial complexities of 2026, sticking to the "old way" of managing debt may no longer be enough.

Stop trading your future for 23% interest. Unlock the value you’ve built in your home and take back control of your monthly cash flow.

Real estate innovator and Managing Partner at PIA Residential and Sell2Rent, boasting over 20 years of experience and 2,000+ units acquired. A Wharton MBA and Forbes contributor, he brings institutional-grade authority to every market insight he shares. Danny’s expertise is further validated by his role on the Planning and Zoning Board for the City of Hallandale, where he helps shape the local landscape. For readers seeking credible, battle-tested advice, Danny offers the perspective of a leader who has successfully navigated decades of market cycles.

Subscribe to the Real Estate Digest. Weekly newsletter.