The Rising Tide of Hidden Homeownership Costs

The narrative of homeownership has long been framed by the monthly mortgage payment. Yet, for a rapidly growing segment of American households, it’s the rising homeownership costs outside of the principal and interest, known collectively as "hidden expenses", that are the primary drivers of financial distress and ultimately, default. This intense financial pressure is forcing vulnerable homeowners to explore extreme measures, from filing for bankruptcy to utilizing strategic financial maneuvers like the sale-leaseback agreement to maintain stability. Understanding these unseen costs and the available relief options is essential for anyone navigating today's complex housing market.

Recent analyses reveal that the average U.S. homeowner is now spending nearly $16,000 annually on essential expenses beyond their average mortgage payment, a staggering burden that is increasing faster than typical household incomes. This phenomenon, where costs spiral out of control, creates the perfect storm for delinquency and foreclosure, demanding urgent attention from both homeowners and the industry according to the National Mortgage Professional.

The Hidden Financial Pressure Cooker of Homeownership

The core of the current default crisis isn't simply high interest rates or home prices, but the escalating price of maintaining a property. When these supplementary costs exceed a family’s budget elasticity, the outcome is unavoidable financial failure.

The Surge in Non-Mortgage Expenses

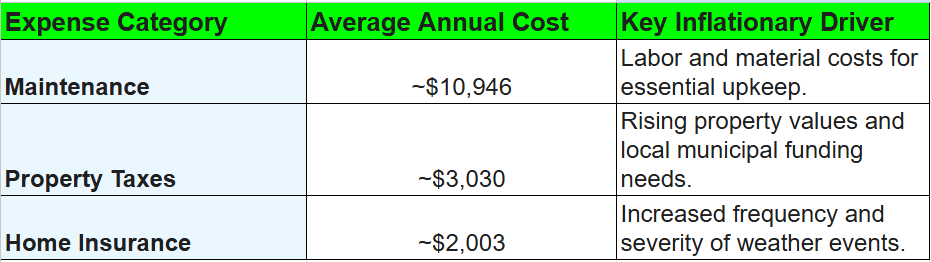

The $15,979 average in annual hidden costs is composed of three major categories: maintenance, property taxes, and home insurance.

The most volatile and damaging component is home insurance. Since February 2020, home insurance premiums have surged by a staggering 48% nationwide. In high-risk areas like certain Florida metros, costs have soared over 70% in five years. This dramatic jump, driven by climate risks and reinsurance costs, adds hundreds, if not thousands, of unexpected dollars to a homeowner’s monthly budget. For homeowners already paying a substantial mortgage, a $400 monthly increase in escrow due to insurance or taxes can be the single factor that tips them into default.

Income Stagnation vs. Cost Inflation

The rate at which these hidden costs are rising, 4.7% year-over-year, is outpacing the 3.8% rise in household incomes over the same period. This growing gap represents a steady erosion of real affordability. As economist Kara Ng noted, these expenses are not just "a budget line item," but a "barrier to entry for aspiring first-time buyers and for families already stretched thin." When a household is already committing a high percentage of its income to housing, any minor financial shock, a job loss, a medical bill, or a sudden insurance hike, can instantaneously render the mortgage unaffordable, initiating the default process.

From Default Notices to the Threat of Bankruptcy

When the pressure cooker of hidden costs explodes, the homeowner is usually left with two paths: fighting to save the home or executing a planned exit. Both options often involve complex legal and financial processes, with bankruptcy being a frequently utilized lifeline.

The Cascade Effect: How $16,000 in Annual Costs Leads to Default

Foreclosure filings have been on the rise, demonstrating the real-world impact of economic pressures. While foreclosures remain below crisis-era peaks, the trend is concerning. Data suggests that a key factor behind the recent increase in foreclosure rates is, indeed, the growing cost of home insurance, utilities, property taxes, and repairs.

These high fixed costs mean that when an unexpected income shock occurs (such as a job loss or disability), the financial system breaks down immediately. Unlike the 2008 crisis driven by predatory lending, today's crisis is often driven by basic economic principles: the monthly outflow exceeds the monthly inflow, leaving no room for error. Roughly 94% of mortgage defaults occur after a homeowner loses income to extenuating circumstances, highlighting the acute vulnerability of those with strained budgets (CBS News, 2025).

Chapter 13 Bankruptcy: A Lifeline for Troubled Mortgages

For many homeowners facing impending foreclosure, filing for Chapter 13 bankruptcy offers an indispensable shield. Chapter 13, often referred to as a "wage earner's plan," allows individuals with regular income to reorganize their finances and propose a repayment plan to creditors over three to five years.

Crucially, filing for bankruptcy triggers the "automatic stay," an injunction that immediately halts foreclosure proceedings, allowing the homeowner critical time to catch up on missed payments (arrearages) through the Chapter 13 plan while continuing to make future payments as they come due. This legal mechanism is vital for homeowners whose inability to pay was caused by a temporary crisis, such as an insurance or tax escrow spike, but who are otherwise financially solvent.

Navigating Foreclosure Alternatives: The Strategic Role of Leaseback

While bankruptcy offers a way to keep the home, some situations require a clean financial break. For those who need to liquidate their equity but wish to remain in their community, the sale-leaseback agreement has emerged as a specialized and effective solution to avoid the long-term credit damage of foreclosure.

What is a Residential Sale-Leaseback Agreement?

A residential sale-leaseback is a financial arrangement where the homeowner sells their property outright to an investor or a leaseback company and simultaneously signs a long-term lease agreement to rent the home back from the new owner.

This transaction accomplishes two critical goals for the financially distressed homeowner:

- Liquidity: The sale provides a lump sum of cash, enabling the homeowner to pay off the existing mortgage (including all past-due amounts) and settle unsecured debts that may have contributed to their overall financial fragility.

- Stability: The homeowner avoids the eviction and credit impact of foreclosure and remains in their home as a tenant, providing family and community stability.

This structure is increasingly appealing to lenders and investors because it allows the borrower to remedy insurmountable mortgage debts without leaving their homes, while avoiding the time and expense of the judicial foreclosure process.

Sell2rent: A Quick, Safe Cash Flow Solution

For homeowners who have built up equity but are struggling to cover the increasing cost burden, especially property taxes, insurance, and maintenance, Sell2rent offers a structured path to a fast, secure sale-leaseback.

Sell2rent utilizes a proprietary digital platform to connect sellers directly with a network of vetted real estate investors interested in purchasing properties through a "Sell & Stay" program. The key benefits for a cash-strapped homeowner include:

- Fast Cash Flow: The process can often close in as little as 15 days, providing rapid access to the home’s equity without the lengthy timeline of a traditional sale. This quick infusion of cash can be used to pay down high-interest debt or cover immediate financial hardships, thereby preventing a potential bankruptcy filing.

- Freedom from Ownership Costs: Once the sale is complete, the responsibility for all those rising costs that triggered the financial strain, property taxes, homeowners insurance premiums, and major capital repairs (like a new roof or HVAC),transfers entirely to the new investor/landlord.

- Safety and Stability: The homeowner remains in their home as a renter, protected by a negotiated lease agreement. This avoids the disruptive and credit-damaging outcome of foreclosure or forced relocation, allowing families to keep their children in the same schools and maintain community ties.

By offering a streamlined, marketplace approach to the leaseback model, Sell2rent provides a critical escape route for homeowners caught between high equity and limited liquidity.

Mitigating Risk: Strategies for Current and Aspiring Homeowners

For the millions of Americans navigating this landscape of rising costs and fragile finances, proactive planning is the only defense against default.

Budgeting for the Unseen: The True Cost of Homeownership

Aspiring and existing homeowners must stop viewing home costs solely as the principal and interest portion of their mortgage. The new rule of thumb requires rigorously budgeting for property taxes, maintenance (reserving at least 1-2% of the home's value annually), and, most critically, a contingency for volatile insurance premiums. Because insurance costs can change dramatically year-to-year based on regional risk assessments, homeowners should treat the escrow component as a variable expense, not a fixed one.

Securing Your Homeownership Future

The data is clear: the main driver of today's mortgage defaults is the escalating, invisible burden of homeownership costs, led by astronomical increases in insurance and taxes. For too long, families have been stretched thin, leaving no cushion to absorb the $16,000 annual cost beyond the mortgage.

Successfully navigating this challenging environment requires a shift toward aggressive financial planning and a deep understanding of defensive mechanisms. Whether through the protective legal shield of Chapter 13 bankruptcy to reorganize debt, the stability offered by a standard leaseback arrangement, or a focused platform like Sell2rent to quickly unlock cash flow and transfer maintenance risks, homeowners have viable options to maintain stability and financial health. The key is to act swiftly and decisively when the first signs of financial strain appear.

Take Control of Your Financial Future.

If you are currently struggling with rising home expenses or facing delinquency, you can Review how a Sell2rent leaseback could provide quick financial relief and stability

Real estate innovator and Managing Partner at PIA Residential and Sell2Rent, boasting over 20 years of experience and 2,000+ units acquired. A Wharton MBA and Forbes contributor, he brings institutional-grade authority to every market insight he shares. Danny’s expertise is further validated by his role on the Planning and Zoning Board for the City of Hallandale, where he helps shape the local landscape. For readers seeking credible, battle-tested advice, Danny offers the perspective of a leader who has successfully navigated decades of market cycles.

Subscribe to the Real Estate Digest. Weekly newsletter.